06 November 2017

How Renewable Energy is Reshaping the Energy Markets

Betting on Renewables: How Renewable Energy is Reshaping the Energy Markets

As the World Yearns for Environmentally Friendly and Sustainable Energy Options, Renewables are Staking Claim to an Ever Increasing Share of the Energy Pie

With renewables making quite a splash in the energy pool, Bear Stearns Research Institute looks at the factors driving the transformation and opportunities arising.

The place of energy in human existence – heating and cooling for industries, buildings and homes; as fuel in transport, and as electricity is indispensable. Thus, the world shall continue to hunger for energy to meet the demands of growing economies and expanding populations desirous of better standards of life. But even as this happens, the reality of climate change and the need for environmental protection demands that reduction of the environmental impact of energy production be a significant preoccupation for society.

It is in this context that the world has increasingly been turning to renewable energy - solar photovoltaic, concentrating solar power, onshore and offshore wind, hydropower, geothermal, bioenergy and ocean tide & wave as choice sources of energy in recent years. 36.9% of renewables are used for electricity and heat production worldwide, while 43.1% are used in the residential, commercial and public sectors (Renewables Information 2018, by the International Energy Agency (IEA)).

It is in this context that the world has increasingly been turning to renewable energy - solar photovoltaic, concentrating solar power, onshore and offshore wind, hydropower, geothermal, bioenergy and ocean tide & wave as choice sources of energy in recent years. 36.9% of renewables are used for electricity and heat production worldwide, while 43.1% are used in the residential, commercial and public sectors (Renewables Information 2018, by the International Energy Agency (IEA)).

Huge Potential Waiting to be Tapped

Exploitable renewable energy resources are to be found all over the world with some regions having particular renewable resources in abundance. Solar resources are the most abundant renewable resource. Photovoltaic (PV) technologies convert sunlight directly to electricity. Concentrating photovoltaic systems collect high temperature heat from solar radiation to drive a steam turbine. Biofuels include fuel wood, bagasse, animal waste, charcoal, liquid biofuels, biogases, industrial waste, and municipal waste. Liquid biofuels are used for transport, electricity generation and run stationary engines. Modern bioenergy was the source of half of all renewable energy consumed in 2017 – four times the contribution of solar photovoltaic (PV) and wind combined. Most modern bioenergy is used in final energy consumption to deliver heat in buildings and for industry. Asia contributes to 39% of world production of biofuels and waste, followed by Africa at 28%, Europe at 13%, Latin America at 11%, North America – 9% and Oceania at 1%. This is a consequence of widespread use of solid biofuels in the residential sector of developing countries. Solar and wind are mostly employed to generate electricity. (Source: Renewables 2018 - IEA market analysis and forecast from 2018 to 2023)

Geothermal power refers to the electricity generated from the heat from geothermal sources – water heated by hot underground rocks to drive a steam turbine. Wind electricity is produced when wind-driven turbines generate electricity. Oceanic wave and tidal energy refers to electricity produced from devices driven by the huge amounts of energy contained in motion of waves and tides. Hydropower supplies the vast majority of renewable electricity, generating 16.3% of world electricity, and 68.4% of total renewable electricity.

Renewables grew by over 4% in 2018 and contributed about a quarter of the growth in primary energy demand in 2018, and accounted for 45% of electricity generation growth. The share of renewable energy in the world’s energy mix is increasing vigorously with the International Energy Agency (IEA) in its report, Renewables 2018, projecting that renewables will grow by 20% and will help meet 12.4% of global energy demand, and provide almost 30% of electricity supply by 2023, increasing from 24% in 2017.

Renewables contribution to heat energy supply will attain 12% in 2023, an increase of 20% since 2017. With current trends, renewables are expected to account for about 18% of global energy supply by 2040. (Source: Global Energy & CO2 Status Report. The latest trends in energy and emissions in 2018).

Geothermal power refers to the electricity generated from the heat from geothermal sources – water heated by hot underground rocks to drive a steam turbine. Wind electricity is produced when wind-driven turbines generate electricity. Oceanic wave and tidal energy refers to electricity produced from devices driven by the huge amounts of energy contained in motion of waves and tides. Hydropower supplies the vast majority of renewable electricity, generating 16.3% of world electricity, and 68.4% of total renewable electricity.

Renewables grew by over 4% in 2018 and contributed about a quarter of the growth in primary energy demand in 2018, and accounted for 45% of electricity generation growth. The share of renewable energy in the world’s energy mix is increasing vigorously with the International Energy Agency (IEA) in its report, Renewables 2018, projecting that renewables will grow by 20% and will help meet 12.4% of global energy demand, and provide almost 30% of electricity supply by 2023, increasing from 24% in 2017.

Renewables contribution to heat energy supply will attain 12% in 2023, an increase of 20% since 2017. With current trends, renewables are expected to account for about 18% of global energy supply by 2040. (Source: Global Energy & CO2 Status Report. The latest trends in energy and emissions in 2018).

And the Factors Playing in Renewables Favor…

Worldwide demand for energy is growing, expanding by 2.3% in 2018, and its fastest pace in a decade, driven by a robust global economy and stronger heating and cooling needs in some regions. The running costs for solar and wind are low as there is no fuel cost. At the same time, continuing improvement in the cost and performance of renewable technologies is contributing to sharp reductions in the capital cost of some renewable technologies. Capital costs continued to fall, by nearly 15% for solar PV and by 5% for onshore wind. Looking ahead in the next few years to 2022, IEA forecasts that costs will drop further by almost a quarter for large, utility-scale solar PV, almost 15% for onshore wind, and a third for offshore wind between 2017-2022 at the global scale. In IEA’s new policy scenario for new utility-scale solar PV and electric vehicle batteries, costs approximately halve from 2016 to 2030. IEA data indicate that renewable projects are breaking new cost competitiveness records, with power purchase agreements for onshore wind and large solar PV farms in several Latin American countries, Middle-East and African countries falling to as low as 33.5 USD/MWh, a level that is very competitive.

On the other hand, the cost of competing (conventional non-renewable technologies) energy sources is increasing. Though the earth’s crust still holds enormous quantities of oil, coal, and natural gas resources, the ongoing depletion of these resources means that cheap, good quality fossil fuels are becoming rarer as the highest-quality, easiest-to-access resources are typically targeted first. During the decade from 2005 to 2015, the oil industry’s costs of production rose by over 10 percent per year. While new extraction technologies make lower-quality resources accessible (like oil from fracking), these technologies require higher levels of investment and usually entail heightened environmental risks.

On the other hand, the cost of competing (conventional non-renewable technologies) energy sources is increasing. Though the earth’s crust still holds enormous quantities of oil, coal, and natural gas resources, the ongoing depletion of these resources means that cheap, good quality fossil fuels are becoming rarer as the highest-quality, easiest-to-access resources are typically targeted first. During the decade from 2005 to 2015, the oil industry’s costs of production rose by over 10 percent per year. While new extraction technologies make lower-quality resources accessible (like oil from fracking), these technologies require higher levels of investment and usually entail heightened environmental risks.

But there are Some Downsides …

Renewables can be influenced by factors such as location, shifts in weather conditions, time of day or season. The challenge in harnessing wind energy is that wind speed is variable and the energy can only be effectively harnessed with high wind speeds. Wind energy also requires large, open expanses of land in order to construct wind farms. Harvesting sun energy fluctuates depending on availability and intensity of radiation from the sun. Biofuels on their part require that a large quantity of crops be grown, necessitating vast areas of agricultural land.

Just like other power plants, renewables also require high investment - the high initial cost of installation and expensive storage systems are major hurdles in the development of renewable energy. Selecting an appropriate site for renewables can be challenging. Sunlight, wind, hydropower, and biomass are more readily available in some places than others. Long-distance transmission entails significant investment costs and energy losses. Moreover, transporting biomass energy resources reduces the overall energy profitability of their use. The small scale of many renewable projects cre¬ates problems in obtaining private financing as many larger financial institutions will be unwilling to consider small projects.

Financial institutions have tended to view financing of energy projects, more so private sector projects, as significantly riskier compared to other types of business projects. Perceived risks including construction, political, project costs uncertainties and high cost of feasibility studies, exchange risk, security risk, and market and country risk. Energy subsidies prevalent in oil and gas exporting countries but also present in importing countries make renewables comparatively more expensive.

Just like other power plants, renewables also require high investment - the high initial cost of installation and expensive storage systems are major hurdles in the development of renewable energy. Selecting an appropriate site for renewables can be challenging. Sunlight, wind, hydropower, and biomass are more readily available in some places than others. Long-distance transmission entails significant investment costs and energy losses. Moreover, transporting biomass energy resources reduces the overall energy profitability of their use. The small scale of many renewable projects cre¬ates problems in obtaining private financing as many larger financial institutions will be unwilling to consider small projects.

Financial institutions have tended to view financing of energy projects, more so private sector projects, as significantly riskier compared to other types of business projects. Perceived risks including construction, political, project costs uncertainties and high cost of feasibility studies, exchange risk, security risk, and market and country risk. Energy subsidies prevalent in oil and gas exporting countries but also present in importing countries make renewables comparatively more expensive.

However, With Some Ingenuity, These Challenges Are Surmountable

In a study, Renewable Electricity Futures, the National Renewable Energy Laboratory of the U.S. Department of Energy explores the challenges that are likely to be encountered in a scenario of high levels of renewable electricity generation. Focusing on a scenario where 80% of all U.S. electricity generation in 2050 comes from renewable sources including wind, solar, hydropower, geothermal and biomass, it observes that at such high levels, the unique characteristics of some renewable resources, specifically geographical distribution and variability and uncertainty in output, pose challenges to the operability of the nation's electric system. Additional challenges to power system planning and operation would arise including management of low-demand periods and curtailment of excess electricity generation. It nevertheless concludes that with a more flexible electric system and the technologies commercially available today, it is feasible to supply 80% of total US electricity generation in 2050 from renewable electricity, including variable wind and solar generation.

Different Regions, Different Tales

Yet, while global demand growth has been strong, there are major disparities across regions. According to the International Energy Agency (IEA), all of the projected growth in energy demand in the next 25 years will take place in emerging and developing countries. In recent years electricity demand in advanced economies has begun to flatten or in some cases decline – electricity demand fell in 18 out of 30 IEA member countries over the period 2010-2017. The key reason is energy efficiency - measures adopted since 2000 saved almost 1800 TWh in 2017, or around 20% of overall current electricity use, with over 40% attributable to energy efficiency in industry.

There are also huge disparities in the contribution and mix of renewables between regions. The world’s major emerging economies – including China, India, and others – are betting heavily on wind, solar and other renewables. In the EU, renewable energy targets and country level policies are helping spur renewables.

There are also huge disparities in the contribution and mix of renewables between regions. The world’s major emerging economies – including China, India, and others – are betting heavily on wind, solar and other renewables. In the EU, renewable energy targets and country level policies are helping spur renewables.

Renewable energy by type, major countries in 2016, 1990 and 2016, and share in total electricity generation, 2016

(Gigawatt hours and percentage)

Of the major energy consumers, Brazil has one of the highest uses of renewable energy with almost 45% of total energy coming from renewables, mainly bioenergy in transport and industry and hydro generated electricity.

China, on account of its deliberate measures to reduce harmful air pollution is leading in terms of absolute growth and is surpassing the European Union to become the largest consumer of renewable energy. China has been particularly active in deploying solar PV contributing 75% of global development of solar PV systems in the five years to 2017 according to Brent Wanner, IEA Energy Analyst. By committing to these new clean technologies, countries like China are helping drive down costs, benefitting the world. IEA forecasts that by 2021, more than one-third of global cumulative solar PV and onshore wind capacity will be located in China.

Hydro 1990 2016 % 2016

China 126,720 1,193,374 19%

Canada 296,848 387,208 58%

Brazil 206,708 380,911 66%

-------------------------------------------------------------------------------------

Wind 1990 2016 % 2016

China 0 237,071 4%

United States 3,066 229,471 5%

Germany 2151991 78,598 12%

-------------------------------------------------------------------------------------

Solar 1990 2016 % 2016

China 0 61,586 1%

Japan 67 50,952 5%

United States 666 50,334 1%

-------------------------------------------------------------------------------------

Total renewables 1990 2016 % 2016

China 126,720 1,531,408 25%

United States 346,434 651,937 15%

Brazil 210,246 470,722 81%

-------------------------------------------------------------------------------------

Of the major energy consumers, Brazil has one of the highest uses of renewable energy with almost 45% of total energy coming from renewables, mainly bioenergy in transport and industry and hydro generated electricity.

China, on account of its deliberate measures to reduce harmful air pollution is leading in terms of absolute growth and is surpassing the European Union to become the largest consumer of renewable energy. China has been particularly active in deploying solar PV contributing 75% of global development of solar PV systems in the five years to 2017 according to Brent Wanner, IEA Energy Analyst. By committing to these new clean technologies, countries like China are helping drive down costs, benefitting the world. IEA forecasts that by 2021, more than one-third of global cumulative solar PV and onshore wind capacity will be located in China.

Focusing on the Most Promising Energy Niche - Electricity

The prospect of renewables is brightest in generation of electricity. Electricity generation more than doubled in the last 27 years — reaching almost 26 000 Terawatt hours (TWh) in 2017. Global electricity demand increased by 3% in 2017 and this is expected to continue, driven by increasing wealth, electrification of end-uses such as heating and mobility, and digitalization. Electricity now accounts for 19% of total final consumption, compared to just over 15% in 2000, and is projected to increase to more than 40 000 TWh in 2040 (IEA’s World Energy Outlook). Ultimately, despite moderate growth in electricity demand, fuel-switching to electricity and energy efficiency improvements in the use of other fuels mean the share of electricity in final consumption is projected to increase to 27% in advanced economies by 2040, up from 22% today

Source: Energy Statistics Yearbook 2019, Department of Economic and Social Affairs, United Nations

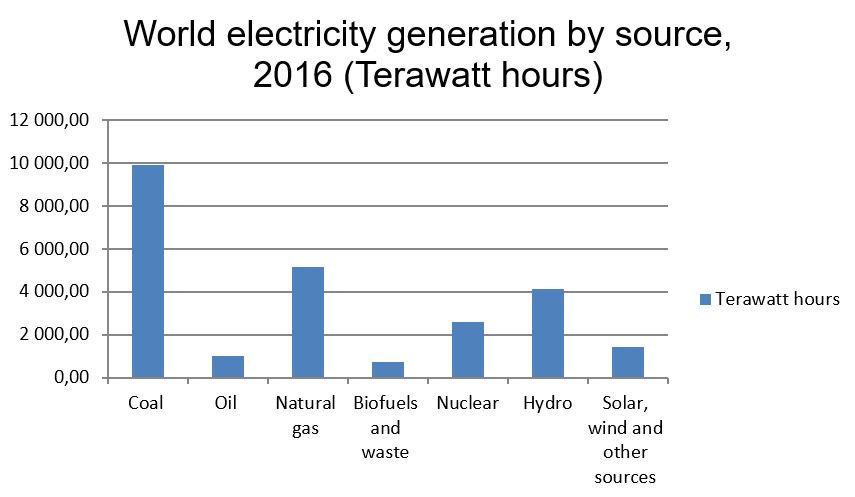

Although growing rapidly, renewables are the second largest contributor to global electricity production accounting for 23.8% of world generation in 2016, after coal (39.2%) and ahead of gas (23.6%), nuclear (10.6%) and oil (3.8%). According to IEA, hydropower is currently the largest renewable source, and will be meeting 16% of global electricity demand by 2023, followed by wind (6%), solar PV (4%), and bioenergy (3%). Biofuels and waste play a minor role in electricity generation. Since 1990, renewable electricity generation worldwide grew on average by 3.7% per annum, which is slightly faster than the total electricity generation average growth rate of 3%. So, whilst 19.4% of global electricity in 1990 was produced from renewable sources, this share increased to 23.8% by 2016. In particular Solar PV and wind have experienced exponential growth in recent years.

Although growing rapidly, renewables are the second largest contributor to global electricity production accounting for 23.8% of world generation in 2016, after coal (39.2%) and ahead of gas (23.6%), nuclear (10.6%) and oil (3.8%). According to IEA, hydropower is currently the largest renewable source, and will be meeting 16% of global electricity demand by 2023, followed by wind (6%), solar PV (4%), and bioenergy (3%). Biofuels and waste play a minor role in electricity generation. Since 1990, renewable electricity generation worldwide grew on average by 3.7% per annum, which is slightly faster than the total electricity generation average growth rate of 3%. So, whilst 19.4% of global electricity in 1990 was produced from renewable sources, this share increased to 23.8% by 2016. In particular Solar PV and wind have experienced exponential growth in recent years.

World electricity generation by source, 1990, 2000, 2010 and 2016

Terawatt hours

Source: Energy Statistics Yearbook 2019, Department of Economic and Social Affairs, United Nations

|

1990 |

2000 |

2010 |

2016 |

Percentage |

Average |

||

|

Source |

share |

Annual increase |

|||||

|

Thermal |

7,696.70 |

10,110.70 |

14,747.80 |

16,796.50 |

67% |

3% |

|

|

- Coal |

4,597.50 |

6,039.60 |

9,009.20 |

9,914.20 |

40% |

3% |

|

|

- Oil |

1,333.80 |

1,324.90 |

1,036.60 |

986.2 |

4% |

-1% |

|

|

- Natural gas |

1,652.00 |

2,539.50 |

4,245.10 |

5,169.80 |

21% |

4.5% |

|

|

- Biofuels and waste |

113.3 |

206.6 |

457 |

726.3 |

3% |

8% |

|

|

Nuclear |

2,019.80 |

2,589.00 |

2,756.30 |

2,608.10 |

10% |

1% |

|

|

Hydro |

2,192.10 |

2,706.60 |

3,528.40 |

4,152.20 |

17% |

2.5% |

|

|

Solar, wind and other sources |

61.6 |

103.9 |

513.8 |

1,431.30 |

6% |

13% |

|

|

Total |

11,970.10 |

15,510.20 |

21,546.30 |

24,988.20 |

100% |

3% |

|

Source: Energy Statistics Yearbook 2019, Department of Economic and Social Affairs, United Nations

Angling for More Accessible and Affordable Energy

Renewables are establishing as an effective means of improving access to affordable energy for populations the world over. Some 900 million people or about 13% of the global population still lacks access to electricity. However, connecting people in remote rural areas in developing countries is daunting - it is expensive to build and maintain grids over vast distances in remote, often with low population densities and difficult terrain. Renewables are proving to be the surer bet to help overcome some of these challenges given the relative abundance of solar, wind and rivers that make it possible to provide electricity to these populations through mini- and off-grid technologies in a more cost effective manner.

Can Renewables Rev Up Transport Through Bioenergy and Electricity?

Renewables have so far failed to make a significant inroad into the transport sector given the continuing dominance of petroleum products. According to IEA, the contribution of renewables in transport grew marginally from 3.4% in 2017 to 3.8% in 2023. Renewables in transport mostly comes from biofuels.

However, as renewables increases their role in electricity, renewable electricity consumption in road (electric cars and buses) and rail transport is projected to increase by 65% over the period 2018 to 2023, though from a low base. Electric mobility is expanding at a rapid pace. In 2018, the global electric car fleet exceeded 5.1 million, up 2 million from the previous year and almost doubling the number of new electric car sales. Electric vehicles on the road in 2018 consumed about 58 terawatt-hours (TWh) of electricity, largely attributable to two/wheelers in China. (Source: Global EV Outlook 2019: Scaling up the transition to electric mobility).

As a result of its considerable use in heat and transport, bioenergy – as solid, liquid or gaseous fuels - has an essential role to play, more so in the transport sector where it helps to decarbonize long-haul transport (aviation, marine and long-haul road freight).

However, as renewables increases their role in electricity, renewable electricity consumption in road (electric cars and buses) and rail transport is projected to increase by 65% over the period 2018 to 2023, though from a low base. Electric mobility is expanding at a rapid pace. In 2018, the global electric car fleet exceeded 5.1 million, up 2 million from the previous year and almost doubling the number of new electric car sales. Electric vehicles on the road in 2018 consumed about 58 terawatt-hours (TWh) of electricity, largely attributable to two/wheelers in China. (Source: Global EV Outlook 2019: Scaling up the transition to electric mobility).

As a result of its considerable use in heat and transport, bioenergy – as solid, liquid or gaseous fuels - has an essential role to play, more so in the transport sector where it helps to decarbonize long-haul transport (aviation, marine and long-haul road freight).

Powering Economies, Reducing Poverty and Transforming Livelihoods

Renewable energy solutions hold the best promise for providing universal, affordable, reliable, cleaner and sustainable energy, particularly to poor and remote rural communities. Access to affordable energy will allow these communities address some of the hardships they face including low quality lighting, polluting fuels such as wood and kerosene, and lack of electricity to power machines and devices. Benefits from the use of renewables include healthier and cleaner environments, mechanization of many production processes, spurring economic activity and job creation. Other conveniences of life that electricity and biofuels facilitate include cooking, heating, refrigeration & cooling, and operation of equipment and appliances in homes, health facilities, schools and offices, in addition to deployment of digital information technologies. As such, renewables are seen as critical for the attainment of Sustainable Development Goal (SDG) 7 which sets a target of universal access to electricity and clean cooking fuels and technologies by 2030.

In agriculture, the major economic sector in most of the developing world, application of energy allows deployment throughout the entire production and marketing chain, of modern technology and equipment which fundamentally improves production, enhances productivity and reduces product spoilage and loss. Improved food production and incomes in turn has ripple positive effects including improved food security, nutrition, and health. Energy also improves access to water by powering water supply systems.

In agriculture, the major economic sector in most of the developing world, application of energy allows deployment throughout the entire production and marketing chain, of modern technology and equipment which fundamentally improves production, enhances productivity and reduces product spoilage and loss. Improved food production and incomes in turn has ripple positive effects including improved food security, nutrition, and health. Energy also improves access to water by powering water supply systems.

Bear Stearns identifies energy as an industry that holds great promise for transforming livelihoods and hence of particular interest as investment in energy systems aligns well with our mantra of ‘making capital work for the benefit of all’. We believe that access to reliable and affordable energy for all will permit radical improvements in productivity and herald prosperity and better quality of life for many.

Towards a Greener Energy Sector

The energy sector is one of the most carbon intensive sectors. The world has its hopes anchored on a shift to widespread use of renewables and application of more efficient technologies to limit carbon and methane emissions. Electricity and heat generation were the largest source of emissions in 2016, accounting for 42% of the global total according to IEA. In the Paris Agreement, nations agreed to limit global warming to no more than two degrees Celsius above preindustrial temperatures. While some of this reduction could technically be achieved by carbon capture and storage from coal power plants, and other technologies and efforts, the great majority of it will require dramatic cuts in fossil fuel consumption.

Society still derives most of its energy from fossil fuels. Every year the amount of carbon dioxide in the atmosphere is increasing by 10.65 billion tons, which is conceived to be the leading contributor to global warming. In 2017, the Energy Sector Carbon Intensity Index increased for the first time in three years as fossil fuels met over 70% of the growth in energy demand according to IEA. While energy intensity – primary energy demand per unit of gross domestic product – has improved over time, this improvement slowed to 1.7% in 2017, compared with an average of 2.3% over the previous three years, and only half the annual improvement rate that would be consistent with delivering the Paris Agreement goals.

In IEA’s estimation, nuclear fission power is not likely to play a larger role in energy future than it does today, outside of China and a few other nations, if current trends continue. High investment and safety requirements, growing challenges of waste storage and disposal, and the risks of accidents may cause significant overall shrinkage of the nuclear industry by the end of the century.

That leaves renewables to shoulder the burden of powering future society and keep a lid on environmental pollution. While significant progress has been made in deploying renewables, in particular solar PV and wind, this has not kept up with energy demand growth. Renewables growing prominence is in electricity generation, but electricity accounts for only a fifth of global energy consumption. The role of renewables in the transportation and heating sectors therefore will remain critical to the energy transition.

According to Adam Brown, Senior Energy Analyst at IEA, modern bioenergy in final global energy consumption should increase four-fold by 2060 in the IEA's 2°C scenario. Bioenergy is expected to deliver on nearly 20% of the additional carbon savings needed to meet announced global environmental policies.

Society still derives most of its energy from fossil fuels. Every year the amount of carbon dioxide in the atmosphere is increasing by 10.65 billion tons, which is conceived to be the leading contributor to global warming. In 2017, the Energy Sector Carbon Intensity Index increased for the first time in three years as fossil fuels met over 70% of the growth in energy demand according to IEA. While energy intensity – primary energy demand per unit of gross domestic product – has improved over time, this improvement slowed to 1.7% in 2017, compared with an average of 2.3% over the previous three years, and only half the annual improvement rate that would be consistent with delivering the Paris Agreement goals.

In IEA’s estimation, nuclear fission power is not likely to play a larger role in energy future than it does today, outside of China and a few other nations, if current trends continue. High investment and safety requirements, growing challenges of waste storage and disposal, and the risks of accidents may cause significant overall shrinkage of the nuclear industry by the end of the century.

That leaves renewables to shoulder the burden of powering future society and keep a lid on environmental pollution. While significant progress has been made in deploying renewables, in particular solar PV and wind, this has not kept up with energy demand growth. Renewables growing prominence is in electricity generation, but electricity accounts for only a fifth of global energy consumption. The role of renewables in the transportation and heating sectors therefore will remain critical to the energy transition.

According to Adam Brown, Senior Energy Analyst at IEA, modern bioenergy in final global energy consumption should increase four-fold by 2060 in the IEA's 2°C scenario. Bioenergy is expected to deliver on nearly 20% of the additional carbon savings needed to meet announced global environmental policies.

For Investors: Opportunities, Optimism, and Some Diligence

While major strides and advances have been achieved, renewable energy technologies are still in their infancy. Vast opportunities exist for investment in construction of new facilities, provision of equipment and in innovation relating to improved, more efficient, more cost-effective energy generation and storage technologies. The U.S. Renewable Electricity Futures study identifies widespread deployment and use of renewable energy, enhancing electric system flexibility, transmission grid expansion, and storage facilities as some of the required areas of investment. Under the 2ºC scenario, up to USD 582 billion per year will be required for investment in new renewable power generation. (World Business Council for Sustainable Development).

In 2017 renewables accounted for a record two-thirds of electricity generation investment supported by a more than 25% expansion in solar PV installations and record growth in offshore wind. As costs continue to fall, energy storage installations have tripled in less than three years, largely driven by lithium ion batteries. Small-scale battery storage is also making inroads, and in off-grid solar applications for energy access, the vast majority of systems now include a storage unit.

Corporate investments in new energy technology companies are growing strongly, reaching their highest ever level of just over USD 6 billion in 2017. The aim is to develop and promote renewable energy technologies and products such as biofuels and biogases to replace oil and other fossil fuels in heating and transport, and provide ICT solutions to the sector (IEA: World Energy Investment 2018- Investing in our energy future)

For private sector financial intermediaries, opportunities exist in devising and deploying suitable financing instruments given the unique features and geo-political risks of renewable energy projects. That way, they can aim to play a bigger role since in many countries, the public sector; international donors and multilateral development banks have taken the lead role in renewable energy investments.

In 2017 renewables accounted for a record two-thirds of electricity generation investment supported by a more than 25% expansion in solar PV installations and record growth in offshore wind. As costs continue to fall, energy storage installations have tripled in less than three years, largely driven by lithium ion batteries. Small-scale battery storage is also making inroads, and in off-grid solar applications for energy access, the vast majority of systems now include a storage unit.

Corporate investments in new energy technology companies are growing strongly, reaching their highest ever level of just over USD 6 billion in 2017. The aim is to develop and promote renewable energy technologies and products such as biofuels and biogases to replace oil and other fossil fuels in heating and transport, and provide ICT solutions to the sector (IEA: World Energy Investment 2018- Investing in our energy future)

For private sector financial intermediaries, opportunities exist in devising and deploying suitable financing instruments given the unique features and geo-political risks of renewable energy projects. That way, they can aim to play a bigger role since in many countries, the public sector; international donors and multilateral development banks have taken the lead role in renewable energy investments.

Looking to the Future

Several factors are likely to impact on the adoption of renewables going forward.

- How far the prices of per unit costs of renewables fall, riding on technology improvements and development of new and cost-effective technologies;

- The relative future competitiveness of fossil fuel prices over time as well as the rate of ongoing trend toward switching away from fossil fuels as seen in the number of existing non-renewable power plants retired and the pace of construction of new non-renewable energy power plants.

- Trends in future energy and electricity demand. The rate of adoption of biofuels in transport and heating as well as the flexibility of industries and other consumers in terms of being able to take advantage of low-cost electricity that would be made available during times of peak renewable energy production and hence ensure fuller use of installed capacities and reduce system costs associated with capacity redundancy, energy storage, and multiple long-distance grid interconnections.

- Investment in additional transmission capacity and the extent of adoption of measures to aggregate the output of dispersed renewables facilities and integrate into the power system;

- The level of private sector involvement and the availability of appropriate funding from private and public sources to raise equity and loans for projects;

- Government incentives and subsidies and standards set by regulators including future carbon prices or subsidies for green energy.

Deliberate Interventions to Define the Clean Energy Future

The rate of innovation and change in renewable energy has been remarkable, driven by desire to achieve universal energy access and cleaner environment. With falling prices and the already strong role of renewables in the energy mix of many countries, and studies indicating that high levels of use and integration of renewables is possible, renewables are likely to play an essential role in meeting the world’s future energy needs. The transition in the world’s energy mix will however demand proper planning, a transformation of electricity systems operation and management; supportive policies, harnessing of advances in renewable technologies and mobilization of adequate and appropriate financing.

Bear Stearns embraces initiatives that drive economic growth and deliver real, sustainable benefits to humanity. You can talk to us on how we can work together to actualize your propositions in energy or other sectors and maximize your returns.

Related reading

06 November 2017

17 May 2019

21 September 2018